DISCLAIMER — Not financial advice. Educational content only, not an offer or solicitation to buy or sell any security. Biotech and small/mid-cap stocks are highly speculative and volatile and can result in a partial or total loss of capital. Do your own research and consult a licensed advisor where appropriate. / Contenuti a solo scopo informativo e didattico, non costituiscono consulenza finanziaria né offerta o sollecitazione al pubblico risparmio ai sensi delle normative CONSOB e SEC. Le azioni biotech e le small/mid cap sono strumenti altamente speculativi e volatili e possono comportare la perdita parziale o totale del capitale investito. Si raccomanda di effettuare sempre le proprie ricerche e, se necessario, di rivolgersi a un consulente abilitato.

Merlintrader Trading Pub

Biotech catalyst news and analysis. FDA PDUFA tracker

Merlintrader Trading Pub

Biotech catalyst news and analysis. FDA PDUFA tracker

Latest Insight

IOVA: technical compression ahead of a real execution catalyst

Iovance is moving into a tight technical zone just as the market prepares for a key Q1 update on Amtagvi, manufacturing, margins and pipeline timing.

On the daily Finviz chart, IOVA is trading near a rising support area while the descending trendline from the March spike is pressing closer from above. The stock has already cooled from the sharp post-February/March momentum move, but it has not yet fully lost the broader higher-low structure that developed after the late-2025 base.

This kind of compression does not predict direction by itself. It simply tells traders that the next real piece of information may matter more than usual. For Iovance, that information is not a binary FDA event. It is the May 7 Q1 2026 corporate update: Amtagvi revenue, gross margin, treatment-center productivity, manufacturing flow, cash runway and any new detail on NSCLC or broader TIL pipeline timing.

The setup is especially interesting because IOVA is no longer just a speculative clinical biotech. Amtagvi is already FDA-approved and generated real 2025 product revenue. The next question is whether the commercial curve is starting to look more repeatable after the 2025 reset.

Trading context: this is a technical and catalyst watch, not a buy signal. The chart is interesting because price is compressing between rising support and descending resistance while a confirmed corporate update is approaching.

IOVA: compressione tecnica prima di un vero catalyst di execution

Iovance sta entrando in una zona tecnica stretta proprio mentre il mercato si prepara a un aggiornamento Q1 importante su Amtagvi, manufacturing, margini e pipeline.

Sul grafico daily Finviz, IOVA sta trattando vicino a un’area di supporto rialzista mentre la trendline discendente partita dallo spike di marzo si avvicina dall’alto. Il titolo si è già raffreddato dopo il forte movimento di febbraio/marzo, ma non ha ancora perso del tutto la struttura di minimi crescenti costruita dopo la base di fine 2025.

Una compressione del genere non predice da sola la direzione. Dice semplicemente ai trader che la prossima informazione concreta potrebbe pesare più del normale. Per Iovance, l’informazione non è una FDA decision binaria. È il corporate update Q1 2026 del 7 maggio: revenue Amtagvi, gross margin, produttività dei treatment centers, flusso manufacturing, cash runway e possibili dettagli su NSCLC o sulla pipeline TIL più ampia.

Il setup è particolarmente interessante perché IOVA non è più solo una biotech clinica speculativa. Amtagvi è già approvato dalla FDA e ha generato product revenue reale nel 2025. La domanda ora è se la curva commerciale stia diventando più ripetibile dopo il reset del 2025.

Contesto trading: questa è una osservazione tecnica e catalyst watch, non un segnale di acquisto. Il grafico è interessante perché il prezzo comprime tra supporto rialzista e resistenza discendente mentre si avvicina un corporate update confermato.

Iovance Biotherapeutics Stock Hub

Iovance Biotherapeutics (Nasdaq: $IOVA): Amtagvi, TIL Therapy, Pipeline, Timeline and Future Catalysts

An evergreen Merlintrader hub for Iovance Biotherapeutics: the first FDA-approved T cell therapy for a solid tumor cancer, the commercial test around Amtagvi, the broader TIL platform, the post-REPL competitive context, the clinical pipeline and the catalyst map traders should keep watching.

Why IOVA matters

Iovance is no longer a purely clinical-stage story. Amtagvi is FDA-approved, commercially launched and positioned in advanced melanoma after anti-PD-1 therapy, making IOVA one of the cleanest public-market tests of whether autologous TIL therapy can become a scalable solid-tumor business.

What the market is testing

The market is not only asking whether TIL biology works. It is asking whether Iovance can convert a complex, individualized therapy into repeatable commercial revenue, improving gross margin, manufacturing flow, ATC utilization and cash runway without losing momentum.

Main risk

The bullish story is real but demanding. Amtagvi is a heavy treatment model, launch expectations were reset in 2025, the company restructured, and the next phase depends on execution, pipeline expansion and the ability to prove that TIL can move beyond melanoma.

Executive summary

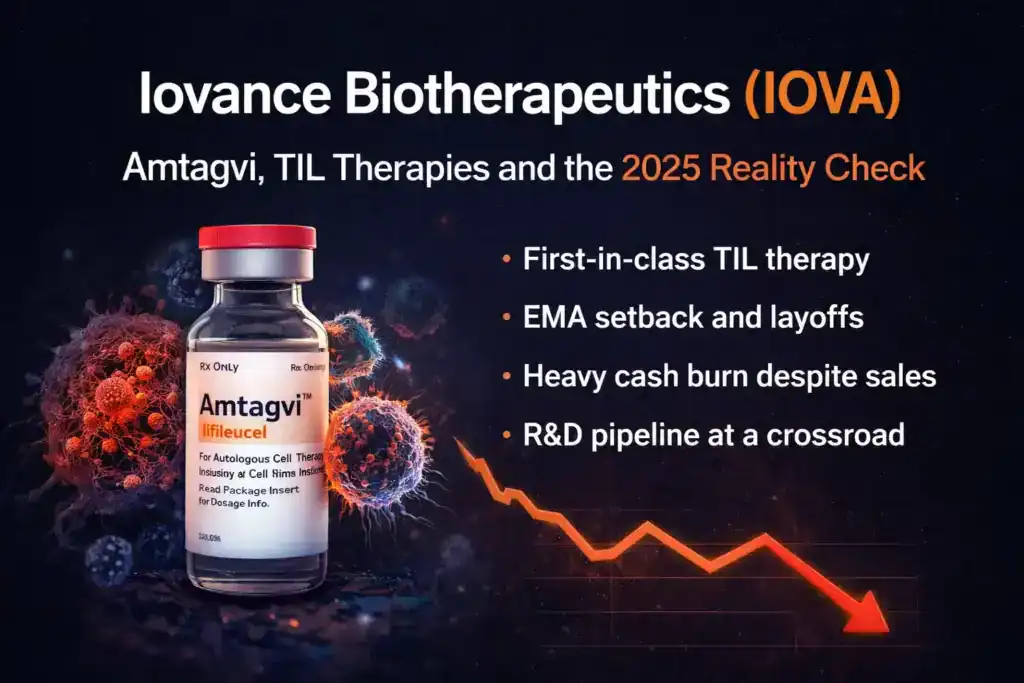

Iovance Biotherapeutics is one of the most important public companies in solid-tumor cell therapy because it has already crossed a line that many oncology platforms never reach: FDA approval. Amtagvi, also known as lifileucel, received accelerated approval from the FDA on February 16, 2024 for adult patients with unresectable or metastatic melanoma previously treated with a PD-1 blocking antibody and, if BRAF V600 positive, a BRAF inhibitor with or without a MEK inhibitor. The approval matters because Amtagvi became the first FDA-approved T cell therapy for a solid tumor cancer and moved tumor-infiltrating lymphocyte therapy from a long academic promise into a real commercial product.

The stock story, however, did not become easy after approval. In fact, the post-approval phase made the story more complicated. Before approval, the dominant risk was regulatory: would FDA allow the first TIL therapy into the market? After approval, the risk became operational: can Iovance manufacture, deliver, reimburse and scale an individualized autologous therapy inside the real-world oncology system? That is the core of the IOVA equity story today. The company has the historic asset. It has the first-mover position. It has an operating commercial infrastructure. But it also has to prove that Amtagvi can become more than a niche high-science product used by a limited number of centers.

This is why IOVA is interesting to a bullish but disciplined reader. The bullish case is not based on vague hope. It is based on a real approval, real product revenue, a maturing network of authorized treatment centers, internal manufacturing, and a pipeline that attempts to extend TIL therapy into NSCLC, endometrial cancer, head and neck cancer, cervical cancer, frontline melanoma combinations and next-generation engineered TIL approaches. The company reported full-year 2025 total product revenue of about $264 million, including about $220 million from U.S. Amtagvi and about $44 million from global Proleukin, and ended 2025 with about $303 million of cash expected to fund operations into the third quarter of 2027.

But the bearish or skeptical case also deserves respect. Iovance lowered expectations in 2025, implemented a restructuring, and had to demonstrate that sales acceleration, gross margin improvement and cost discipline could repair confidence. A therapy with tumor resection, centralized manufacturing, lymphodepletion, IL-2 support and specialized center logistics is not a standard oncology pill or simple infusion. The product may be clinically differentiated, but the commercial model is heavy. A lot of the valuation depends on whether the company can make the pathway more repeatable, bring more patients into the system earlier, and use the existing infrastructure to support additional indications.

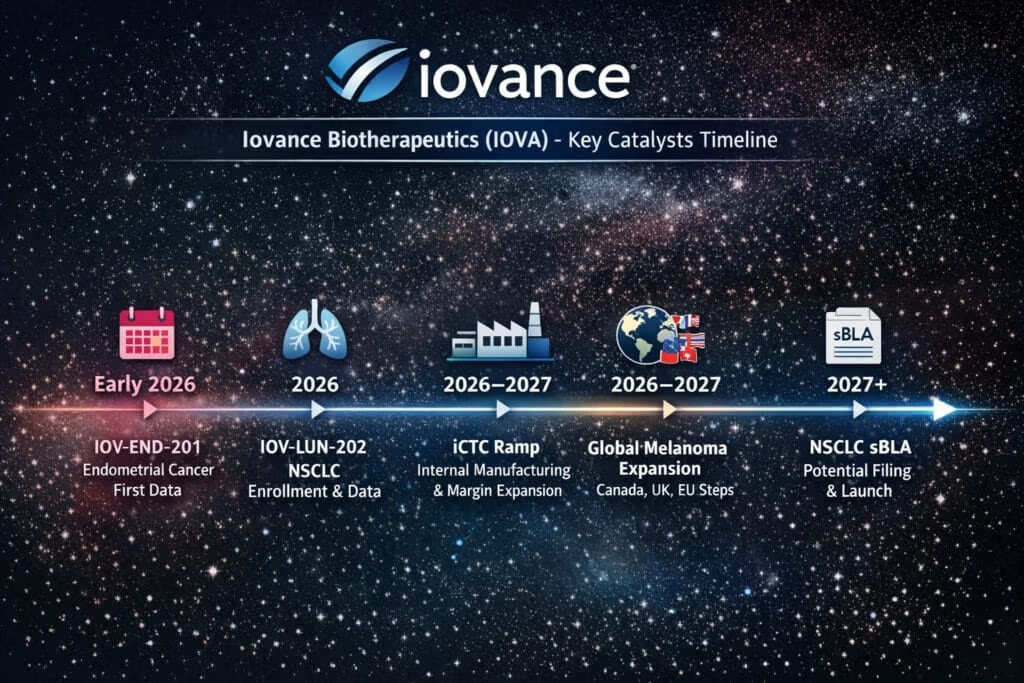

The most important near-term catalyst is the May 7, 2026 first-quarter 2026 financial results and corporate update. This is not a binary FDA event. It is an execution checkpoint. Investors should watch Amtagvi revenue, Proleukin contribution, gross margin, manufacturing turnaround, ATC activity, international progress, cash runway, and any updated commentary on NSCLC, endometrial cancer, frontline melanoma and next-generation TIL. The most important medium-term catalyst is probably NSCLC. If Iovance can build a credible registrational path in lung cancer, the story moves from “approved melanoma cell therapy” to “platform expansion into one of the largest solid-tumor markets.”

Merlintrader editorial view. IOVA can be approached with a constructive bias without turning it into promotion. The company owns a historically important approval and a potentially expandable platform. The correct framework is not “risk-free winner,” but “commercial-stage cell-therapy platform where execution now decides whether the first approval becomes the foundation of a broader solid-tumor franchise.”

Fast snapshot

| Field | Current read |

|---|---|

| Company | Iovance Biotherapeutics, Inc. |

| Ticker | $IOVA, Nasdaq |

| Core therapy | Amtagvi / lifileucel, a tumor-derived autologous T cell immunotherapy. |

| Approved indication | Unresectable or metastatic melanoma after anti-PD-1 therapy and, if BRAF V600 positive, after BRAF-targeted therapy with or without MEK inhibition. |

| Regulatory status | FDA accelerated approval granted February 16, 2024; continued approval may depend on verification of clinical benefit. |

| 2025 revenue base | About $264 million total product revenue: about $220 million U.S. Amtagvi and about $44 million global Proleukin. |

| Cash runway | Cash position of about $303 million as of December 31, 2025, expected to fund operations into Q3 2027, according to the company. |

| Core pipeline expansion | NSCLC, frontline melanoma combinations, endometrial cancer, cervical cancer, head and neck cancer, engineered TIL and next-generation cytokine approaches. |

| Nearest catalyst | Q1 2026 financial results and corporate update scheduled for May 7, 2026 at 8:30 a.m. ET. |

The central thesis: IOVA is an execution story now

The easiest mistake with IOVA is to keep reading it like a pre-approval biotech. That version of the story is over. The company already achieved the milestone that made the platform impossible to ignore: the FDA allowed an autologous TIL therapy into the market for a solid tumor. The current question is different. It is whether Iovance can convert that regulatory win into a durable business while preserving enough capital and pipeline momentum to expand beyond the first label.

That shift is important for traders and long-term readers because the catalyst structure changes. Before approval, the stock could be dominated by FDA documents, PDUFA sentiment, advisory-committee speculation and binary-event positioning. After approval, the stock is judged quarter by quarter. Revenue matters. Gross margin matters. Manufacturing turnaround matters. The number and maturity of authorized treatment centers matter. Community oncology referrals matter. Payer friction matters. Operating expenses matter. The slope of patient adoption matters. The company can no longer win the narrative only by showing that the science is impressive. It has to show that the therapy can move through the healthcare system repeatedly.

This is also where the bullish view becomes more mature. A bullish IOVA thesis does not need to pretend that the launch has been effortless. It was not. The company had to lower its 2025 revenue expectations, cut costs and defend runway. But the same period also showed that the company could still generate meaningful product revenue, reach its revised guidance range, improve gross margin and continue pushing the pipeline. That is the more interesting setup: not a clean, straight-line commercial success, but a high-friction launch that may still be moving toward a more investable model if the operational curve improves.

For an evergreen hub, the bottom line is this: IOVA is one of the rare biotech names where the debate is not whether the platform is real in principle. The FDA approval, the prescribing information, the commercial revenue and the maturing infrastructure answer that first question. The debate is whether the platform is scalable enough to support a company value meaningfully above a single-product niche oncology story. That is why every future update should be read through four lenses: commercial adoption, manufacturing efficiency, pipeline expansion and cash discipline.

Amtagvi explained: what the product actually is

Amtagvi is not a conventional drug. It is an individualized, tumor-derived autologous T cell immunotherapy. In practical terms, the treatment begins with a patient’s own tumor tissue. Tumor-infiltrating lymphocytes are extracted, expanded outside the body, and then returned to the patient after preparative lymphodepletion, followed by IL-2 support. This is a very different model from antibody therapy, checkpoint inhibition, oral targeted therapy or standard chemotherapy. The therapy is personalized to each patient, which is one reason the biology is compelling and also one reason the logistics are demanding.

The clinical logic behind TIL therapy is attractive. Tumors already contain immune cells that have recognized the cancer. The challenge is that, inside the tumor microenvironment, those cells may be insufficient in number, suppressed, exhausted or unable to mount a durable response. TIL therapy attempts to harvest the immune recognition that already exists, expand it massively, and return it to the patient in a form that can attack the tumor more forcefully. This is why Iovance’s platform is viewed as a potential bridge between personalized immunology and industrial cell-therapy manufacturing.

The approved setting is advanced melanoma after prior anti-PD-1 therapy, and if BRAF V600 mutation positive, after BRAF-targeted therapy. That matters because this is a population with limited remaining options and a large unmet need. Checkpoint inhibitors transformed melanoma treatment, but not every patient responds, and many eventually progress. Amtagvi sits in the difficult post-checkpoint space where durable response can be highly valuable even if treatment is intensive.

The accelerated approval was based on objective response rate, and the label makes clear that continued approval may be contingent upon verification and description of clinical benefit in a confirmatory trial. This is not unusual for accelerated approvals, but it is important. IOVA is commercial, but the regulatory story is still alive. The confirmatory and expansion programs are not optional decoration. They are part of the long-term regulatory and strategic architecture of the franchise.

Timeline: from research platform to commercial-stage biotech

| Period | Milestone | Why it matters |

|---|---|---|

| Academic foundation | TIL therapy was developed from a long scientific history including work at the National Cancer Institute and academic cancer centers. | This gave Iovance a platform rooted in decades of immuno-oncology research rather than a purely speculative new modality. |

| Pre-approval development | Iovance built multicenter trials, proprietary manufacturing processes, bioanalytical platforms and the infrastructure needed to industrialize TIL therapy. | The company’s value proposition became not only the therapy itself, but the ability to make TIL commercially deliverable. |

| February 16, 2024 | FDA granted accelerated approval to lifileucel / Amtagvi in advanced melanoma after anti-PD-1 therapy. | This was the defining event: the first FDA-approved T cell therapy for a solid tumor cancer. |

| 2024 launch year | Iovance began the U.S. commercial launch while building the authorized treatment center network and marketing Proleukin. | The story moved from binary regulatory risk to commercial execution. |

| 2025 reset | Revenue expectations were reduced and the company implemented restructuring to improve cost discipline and runway. | This was the major credibility test of the launch: the product was real, but commercial adoption was harder than initial expectations. |

| FY2025 results | Iovance reported about $264 million in total product revenue, Q4 revenue of about $87 million, Q4 gross margin of about 50%, and cash expected to fund operations into Q3 2027. | The company showed that the launch remained alive after the reset and that cost actions could support runway. |

| May 7, 2026 | Q1 2026 financial results and corporate update. | This is the next execution checkpoint for revenue, margin, ATC maturity, pipeline timing and cash runway. |

Commercial story: what needs to work

Amtagvi’s commercial ramp has several moving parts. The first is patient identification. Advanced melanoma patients who have progressed after checkpoint therapy may be treated across a wide network of oncologists, but not all of those physicians are deeply familiar with TIL therapy. Iovance needs education, referral pathways and center relationships. A patient may start with a community oncologist and then need referral to an authorized treatment center capable of managing the procedure. That creates more friction than a therapy that can be prescribed and administered locally without complex coordination.

The second moving part is treatment-center activation and maturity. Simply listing authorized treatment centers is not enough. The real question is how many centers are referring, resecting, manufacturing and infusing patients repeatedly. Early in a launch, many centers exist on paper but contribute limited volume. Over time, the bullish commercial case requires more centers to become productive, more physicians to build confidence, and more teams to understand the operational flow. This is why the company’s commentary about academic ATCs, community ATCs, patient proximity and experienced centers matters so much.

The third moving part is manufacturing. Iovance has emphasized the Iovance Cell Therapy Center and the internalization of lifileucel manufacturing. This is central to the business model. If manufacturing is slow, expensive or unpredictable, revenue growth becomes harder and gross margin is constrained. If turnaround improves, cost of sales improves, and the company can treat more patients with fewer bottlenecks, the commercial model becomes more attractive. The company has cited manufacturing turnaround of 32 days or less from inbound to return shipment to ATCs, which is one of the operational metrics to keep monitoring.

The fourth moving part is reimbursement and patient access. Amtagvi is a high-value, high-complexity therapy. Reimbursement must support both the product and the treatment pathway. The company needs payor confidence, hospital workflow support and an access process that does not discourage eligible patients. Strong reimbursement does not eliminate friction, but it makes the system more repeatable. Weak reimbursement or operational confusion would slow the ramp even if the clinical logic is strong.

The fifth moving part is the clinical message. Iovance has highlighted real-world response rates and the importance of earlier treatment. If physicians believe that patients do better when they reach Amtagvi earlier after fewer prior lines of therapy, the company may be able to influence referral behavior. This matters because cell therapy often suffers when patients are referred too late, after disease progression or declining performance status makes intensive treatment more difficult. A major commercial goal is therefore not only to increase awareness, but to move referral timing earlier in the treatment journey.

Financial snapshot and runway

The most important financial update before Q1 2026 is the full-year 2025 report. Iovance reported fourth-quarter 2025 total product revenue of approximately $87 million, up about 30% from the prior quarter, including approximately $65 million of U.S. Amtagvi revenue and approximately $22 million of global Proleukin revenue. For the full year, total product revenue was approximately $264 million, including approximately $220 million from U.S. Amtagvi and approximately $44 million from global Proleukin. The company also reported fourth-quarter gross margin from cost of sales of approximately 50%, reflecting operational execution and cost optimization.

These numbers matter for two reasons. First, they show that Amtagvi is not an approval without revenue. The product is generating real sales. Second, they show that the launch still needs scale. A $220 million U.S. Amtagvi year is meaningful for a first full launch year in a complex therapy category, but it does not by itself prove that Iovance has already built a high-margin, self-sustaining oncology franchise. The next phase has to show whether revenue can keep growing while operating expenses and manufacturing costs move in the right direction.

The cash position is also central. Iovance reported approximately $303 million of cash as of December 31, 2025, and said that this position was expected to fund operations into the third quarter of 2027. That runway is important because the company still needs to execute launch growth and advance pipeline studies. Biotech investors are always sensitive to dilution risk, but the FY2025 update gave the company a clearer window to execute before the next major financing question becomes urgent.

The financial bull case is straightforward: continued revenue growth, improving gross margin and controlled spending can extend credibility and reduce financing pressure. The financial bear case is also straightforward: if revenue stalls, margin gains fade or pipeline spending remains heavy, cash runway can become a renewed overhang. The May 7 Q1 2026 update should therefore be read less as a simple earnings print and more as a health check on the entire operating model.

Pipeline map: where IOVA can become more than Amtagvi melanoma

Iovance’s biggest strategic question is whether TIL therapy can scale beyond the first approved melanoma indication. If the answer is no, IOVA remains a specialized commercial oncology company with a historically important but limited product. If the answer is yes, the company becomes something much more ambitious: a platform capable of entering multiple solid tumors with several generations of TIL products and combinations.

NSCLC: the highest-impact expansion path

Non-small cell lung cancer is the most important pipeline expansion area because it is a large market and because post-checkpoint disease remains a difficult treatment setting. Iovance’s pipeline includes lifileucel and LN-145 approaches in NSCLC, including IOV-LUN-202 cohorts and Gen 3 manufacturing concepts. The company has described positive interim data and potential registrational paths, and the market will continue watching enrollment, response rates, durability, safety, manufacturing feasibility and the timing of any potential supplementary BLA strategy.

For traders, NSCLC is the catalyst that could change the scale of the company. Melanoma validates the platform. Lung cancer could expand the platform into a much larger commercial discussion. The risk is that NSCLC is biologically and operationally difficult; signals need to be strong enough to justify treatment complexity. A modest signal may not be enough. A compelling signal could re-rate the entire platform.

Frontline melanoma combinations

Iovance is also studying lifileucel in combination settings, including frontline advanced melanoma with pembrolizumab through TILVANCE-301. This matters because earlier-line treatment may improve outcomes and potentially increase eligible patient volumes. It also matters for the accelerated approval architecture: confirmatory studies and earlier-line strategies can support the long-term regulatory standing and commercial reach of Amtagvi.

Endometrial cancer, cervical cancer and head and neck cancer

The pipeline includes endometrial cancer after anti-PD-1, cervical cancer combinations and head and neck squamous cell carcinoma settings. These indications are important because they test whether TIL therapy can move through multiple immunologically relevant solid tumors. Some of these programs may not be as immediately valuation-driving as NSCLC, but they help define the breadth of the platform. For an evergreen hub, they should be tracked as optionality, not as guaranteed value.

Next-generation TIL and engineered approaches

Iovance is also developing next-generation approaches, including PD-1 inactivated TIL such as IOV-4001, PBL therapy, Gen 3 manufacturing and next-generation cytokine support. This is where the long-term platform story becomes more speculative but potentially powerful. The goal is to improve potency, persistence, manufacturing, safety or treatment experience. Investors should treat these assets as early platform upside until data mature.

Pipeline takeaway. Amtagvi approval proves that Iovance can bring TIL therapy to market. NSCLC and frontline melanoma will test whether the platform can become broader. Engineered TIL and next-generation cytokines will test whether the company can keep innovating rather than depending on the first generation of the platform.

Future catalyst map

| Catalyst | Timing / status | Why it matters |

|---|---|---|

| Q1 2026 financial results and corporate update | May 7, 2026 at 8:30 a.m. ET | Key execution checkpoint for Amtagvi revenue, Proleukin revenue, gross margin, cash runway, ATC activity and pipeline timing. |

| Amtagvi commercial ramp | Quarterly | Revenue growth, patient starts, ATC productivity, referral patterns and reimbursement flow determine whether approval becomes a scalable business. |

| Manufacturing and iCTC efficiency | Ongoing | Turnaround, cost of sales and internal manufacturing execution drive gross margin and capacity confidence. |

| NSCLC / IOV-LUN-202 updates | Ongoing / future clinical and regulatory updates | The highest-impact pipeline expansion path; a credible lung cancer strategy could change the scale of IOVA. |

| Frontline melanoma confirmatory / combination work | Ongoing | Important for the long-term regulatory and commercial architecture of the melanoma franchise. |

| Endometrial and cervical cancer data | Future clinical updates | Tests whether TIL therapy can expand into additional solid tumors beyond melanoma and NSCLC. |

| UK and Australia regulatory progress | Potential approvals were anticipated in H1 2026 according to company commentary | International launches could broaden the revenue base and validate ex-U.S. demand. |

| EMA strategy | Company working on resubmission strategy after withdrawing the prior MAA in 2025 | Europe remains important but requires careful regulatory reconstruction. |

| Next-generation TIL / IOV-4001 updates | Future early data | Potential long-term platform upside, but still early and data-dependent. |

The REPL comparison: useful, but not simplistic

Replimune’s second Complete Response Letter for RP1 plus nivolumab in advanced melanoma makes IOVA more relevant in the competitive discussion, but the comparison must be handled carefully. REPL and IOVA sit in the same clinical neighborhood because both address advanced melanoma after checkpoint therapy. However, the treatment models are very different. RP1 was an intratumoral oncolytic immunotherapy proposal. Amtagvi is an approved autologous cell therapy requiring tumor procurement, manufacturing, lymphodepletion and IL-2 support.

The useful read-through is not that Iovance automatically captures every patient that Replimune might have served. That would be too simplistic. Some patients who might have been candidates for an injectable intratumoral approach may not be ideal candidates for a complex cell therapy. The useful read-through is that Iovance gains narrative centrality because it is already approved and commercially active in a high-unmet-need post-PD-1 melanoma setting. When a near-market competitor is delayed or weakened, the approved product becomes more central in investor conversations.

This matters because IOVA’s story is partly about category leadership. In a field where multiple oncology platforms are trying to show relevance in solid tumors, being first matters. But being first is only an advantage if the company can keep executing. The REPL setback helps the relative narrative, but the IOVA thesis still depends on Amtagvi ramp, manufacturing economics, confirmatory work and pipeline expansion.

CEO, management and execution

Iovance’s management section deserves more than a quick biography because the company is now being judged less like a discovery-stage biotech and more like a commercial-stage execution platform. The leadership question is not only whether the science team understands TIL biology. It is whether the organization can coordinate manufacturing, medical affairs, payer access, center training, clinical development, international regulatory strategy and capital allocation while running a complex launch.

Frederick G. Vogt, Ph.D., J.D., has served as Interim President and Chief Executive Officer since 2021 and has also served on the board of directors. He originally joined Iovance in 2016 and previously held senior legal and corporate roles at the company, including General Counsel. His profile is unusual for a commercial-stage biotech CEO because it combines legal, regulatory and corporate development experience with a long internal operating history at Iovance. That can be a strength in a company where regulatory strategy, intellectual property, manufacturing agreements, payer infrastructure and partnership optionality all matter. The counterpoint is that “interim” leadership has remained part of the IOVA story for a long time, and long-term investors may reasonably want to see whether the board eventually formalizes or changes the leadership structure as the company matures commercially.

The broader executive team is also important. The Q4 2025 call participants included Chief Financial Officer Corleen Roche, Chief Commercial Officer Daniel G. Kirby, Chief Operating Officer Igor P. Bilinsky, Chief Medical Officer Friedrich Graf Finckenstein, Executive Vice President of Clinical Development Brian Gastman, Head of Regulatory and Translational Medicine Raj K. Puri and commercial operations leadership. That mix reflects the nature of the company: IOVA is not only a clinical biotech, and it is not only a sales story. It is a manufacturing, clinical, regulatory, commercial and financial execution story at the same time.

For investors, the management scorecard should focus on measurable execution rather than inspirational language. The first item is commercial transparency: management needs to give enough detail on Amtagvi revenue, patient demand, center productivity, referral behavior and payer friction to let the market understand whether the launch is improving. The second item is manufacturing discipline: turnaround time, internal manufacturing utilization, gross margin and cost of sales will say more about the platform’s commercial viability than broad statements about demand. The third item is pipeline prioritization: NSCLC, frontline melanoma, endometrial cancer and next-generation TIL cannot all be equally central at every moment. The market needs to understand where capital is being concentrated.

The 2025 restructuring was one of the clearest tests of management credibility. It showed that the company was willing to adjust expenses after the launch curve disappointed, rather than simply spending through a slower ramp. For bullish readers, that can be read as discipline: management adapted to reality and preserved runway into Q3 2027. For skeptical readers, the same event can be read as evidence that the original launch assumptions were too optimistic. Both readings are fair. What matters now is whether the post-restructuring model produces better operating leverage in 2026.

The management section should therefore be updated after every major earnings call. The most useful questions are practical: Did management quantify the launch better than before? Did gross margin improve? Did the company maintain or extend runway? Did it provide clearer NSCLC timing? Did it explain international regulatory strategy in a way that reduces uncertainty? Did it avoid overpromising? IOVA does not need promotional management language. It needs repeatable execution metrics.

Institutional ownership, insider context and retail sentiment

IOVA remains a heavily followed biotechnology stock with a shareholder base that mixes specialist healthcare investors, large index and asset-management firms, event-driven biotech investors and active retail traders. Aggregated 13F-style data should always be treated as delayed and imperfect, but current ownership screens show institutional interest remains material. Fintel, for example, lists hundreds of institutional owners and identifies large holders such as BlackRock, MHR Fund Management, Vanguard, State Street, Bank of America, Invenomic Capital Management, Morgan Stanley, Goldman Sachs, Long Focus Capital Management and Geode Capital Management among the reported holder base.

The presence of large institutions is not, by itself, a bullish guarantee. In biotech, institutional ownership can reflect index exposure, passive ownership, legacy positions, specialist risk-taking, hedged strategies or delayed 13F reporting. The more useful question is not simply “are institutions present?” but whether specialist healthcare investors are adding, reducing or staying patient as the commercial ramp develops. Any future update to this hub should check the latest 13F changes, 13D/13G filings, insider Form 4 activity and updated proxy ownership tables before drawing conclusions.

Insider context should also be handled carefully. Insider buying can be a strong signal when it is open-market, meaningful and not driven by automatic plans. Insider selling can be less informative when it is tax-related or plan-based. Because IOVA is a volatile commercial biotech, ownership and insider data should not be used as standalone proof of conviction. They are supporting evidence only. The fundamental story still rests on revenue, margin, pipeline progress and runway.

Retail sentiment is naturally more emotional. Bulls tend to emphasize that Amtagvi is already FDA-approved, that the therapy is first-in-class for a solid tumor, that Replimune’s second CRL makes Iovance more central in the post-PD-1 melanoma conversation, and that NSCLC could materially expand the opportunity. Bears and skeptics focus on the 2025 reset, treatment complexity, dilution risk, launch friction and the possibility that TIL remains too operationally heavy for broad adoption.

The right editorial approach is to treat retail sentiment as a temperature gauge, not as evidence. It can help explain volatility, option activity and social-media attention, but it cannot verify clinical efficacy, regulatory probability or commercial demand. For Merlintrader readers, the clean framework is this: institutional activity may show whether professional money is staying engaged; insider activity may reveal management alignment if transactions are meaningful; retail sentiment can amplify the move; but the durable driver remains Amtagvi execution and pipeline validation.

Analyst coverage and Wall Street expectations

Analyst coverage is important for IOVA because the stock sits at the intersection of commercial biotech, cell therapy, oncology launch execution and pipeline optionality. The consensus view can change quickly after revenue updates, margin surprises, guidance changes or new clinical data. As of early May 2026, public analyst-rating aggregators generally show a constructive but cautious Wall Street setup: the average price target is above the current share price, but the range of targets is wide, reflecting disagreement over how large Amtagvi can become and how much value to assign to NSCLC and other pipeline expansion opportunities.

One public aggregation source, MarketBeat, listed 12 analyst price targets with an average around $8.88, a high target of $16 and a low target of $2. That range is more useful than the average. A wide target spread tells readers that the Street is not simply debating a small quarterly miss or beat. Analysts are debating the shape of the entire commercial model. The low end reflects concern that Amtagvi may remain niche and capital-intensive. The high end reflects the possibility that the launch improves, gross margins expand, and the pipeline creates meaningful optionality beyond melanoma.

Analysts will likely focus on four variables in the Q1 2026 and subsequent updates. First, Amtagvi revenue: not just the absolute number, but the sequential growth rate and the quality of demand. Second, margin: whether internal manufacturing and cost optimization are visibly improving the financial profile. Third, cash runway: whether the company can preserve the Q3 2027 runway while still funding pipeline work. Fourth, pipeline timing: especially NSCLC, because that is the most obvious indication that can change the company’s scale if the data and regulatory path become credible.

For readers, analyst targets should be treated as scenario markers, not truth. A bullish target does not make the stock safe, and a bearish target does not invalidate the platform. The value of analyst coverage is that it reveals what the market is likely to react to. In IOVA’s case, the checklist is fairly clear: revenue acceleration, ATC productivity, manufacturing economics, pipeline updates and financing risk. If the company improves those metrics, analyst revisions can become a tailwind. If the metrics disappoint, the same coverage can pressure sentiment quickly.

Bull case

The bullish case for IOVA begins with the most important fact: the platform has already produced an FDA-approved product in a solid tumor. Many oncology stories never get that far. Amtagvi gives Iovance a real commercial base, a differentiated clinical identity and a first-mover position in TIL therapy. If revenue continues to grow, gross margin improves and ATC productivity rises, the market may begin to treat IOVA less like a failed launch story and more like a difficult launch that is starting to mature.

The second bullish pillar is pipeline expansion. NSCLC is the big one. A credible path in lung cancer could materially expand the addressable opportunity and transform the company’s narrative. Frontline melanoma combinations could defend and enlarge the melanoma franchise. Endometrial, cervical and head and neck programs provide additional platform optionality. Next-generation TIL and cytokine programs could eventually improve potency, manufacturing or tolerability.

The third bullish pillar is operating leverage. If internal manufacturing, cost optimization and disciplined spending continue to improve the financial profile, the company may gain time to reach the next value-creating clinical events. The FY2025 update showed improving Q4 gross margin and a runway into Q3 2027. That does not remove financing risk forever, but it creates a clearer execution window.

Bear case and red flags

The bear case is that Amtagvi remains too complex to scale broadly. An individualized therapy that requires tumor resection, manufacturing, lymphodepletion, IL-2 support and specialized care can be clinically powerful but commercially difficult. If patient flow remains slower than expected, the product could remain a specialized therapy rather than a large oncology franchise.

The second red flag is that pipeline expansion is not guaranteed. NSCLC may be large, but it is also hard. Signals must be compelling enough to justify treatment complexity. Earlier-line combinations require strong evidence and may face competitive pressure from established immuno-oncology regimens. Next-generation programs are promising but still early.

The third red flag is capital. Iovance has runway, but it is still a biotech with ongoing R&D, commercial infrastructure and manufacturing needs. If revenue disappoints or trials require more investment, dilution risk can return. The fourth red flag is international regulation. Canada was a positive step, but the EU path required a reset after the MAA withdrawal, and ex-U.S. commercialization is not automatic.

Risk summary. The IOVA story is bullish only if execution improves. Approval alone is not enough. The company must prove that Amtagvi can grow, that manufacturing can scale, that cash can last, and that the pipeline can create credible second and third acts.

Merlintrader bottom line

Iovance is one of the most compelling and difficult biotech stories in the public market. It is compelling because the company has already done something historic: bring the first FDA-approved T cell therapy for a solid tumor cancer to market. It is difficult because the next stage is not a simple science question. It is an execution question that combines manufacturing, hospital workflow, payers, physicians, patients, cash management and clinical expansion.

A balanced but constructive view is appropriate. The platform has real credibility. Amtagvi is not theoretical. The revenue base is real. The pipeline has meaningful optionality, especially in NSCLC. The competitive setup after REPL’s second CRL makes IOVA more central in the post-PD-1 melanoma discussion. But the company still has to prove that the commercial model can scale and that the next wave of data can support broader use.

For traders, $IOVA should be treated as a catalyst-rich commercial biotech, not a simple binary PDUFA stock. The key checkpoints are quarterly Amtagvi revenue, ATC productivity, manufacturing margin, cash runway, NSCLC updates, international approvals and management’s ability to communicate a disciplined plan. If those pieces improve together, the bullish story can strengthen without needing promotional language. If they diverge, volatility can return quickly.

Primary and reference sources

- FDA — Accelerated approval of lifileucel / Amtagvi for unresectable or metastatic melanoma

- FDA — AMTAGVI approval history, letters, reviews and supporting documents

- FDA — AMTAGVI prescribing information

- Iovance — Q4 and full-year 2025 results, business achievements and corporate update

- SEC / Iovance 8-K exhibit — FY2025 financial highlights and commercial update

- Iovance — Official immuno-oncology pipeline

- Iovance — Clinical trials page

- Iovance Form 10-Q for quarter ended September 30, 2025

- Iovance — Q1 2026 results and corporate update date

Biotech Catalyst Calendar

Track upcoming FDA, trial and biotech market catalysts with the Merlintrader calendar.

Open the Biotech Catalyst CalendarDisclaimer

This content is for informational, educational and editorial purposes only. It is not financial advice, not a solicitation to invest and not a recommendation to buy or sell any security. Biotech equities can be highly volatile, clinical and regulatory outcomes are uncertain, and commercial execution can change quickly. Interpretive sections reflect editorial analysis based on public sources and may become outdated as new filings, data, regulatory decisions or corporate updates emerge.

Legal and informational pages: Merlintrader Disclaimer | Terms of use and privacy

Perché IOVA conta

Iovance non è più una storia puramente clinica. Amtagvi è approvato dalla FDA, commercializzato e posizionato nel melanoma avanzato dopo terapia anti-PD-1: questo rende IOVA uno dei test pubblici più chiari sulla possibilità di trasformare la TIL therapy autologa in un business scalabile nei tumori solidi.

Cosa sta testando il mercato

Il mercato non chiede solo se la biologia TIL funzioni. Sta chiedendo se Iovance possa trasformare una terapia personalizzata complessa in ricavi ripetibili, con margine lordo migliore, flusso produttivo più efficiente, maggiore utilizzo degli ATC e runway difendibile.

Rischio principale

La storia costruttiva è reale ma esigente. Amtagvi è un modello terapeutico pesante, le aspettative di lancio sono state resettate nel 2025, la società ha ristrutturato e la prossima fase dipende da execution, pipeline e capacità di provare che TIL possa andare oltre il melanoma.

Executive summary

Iovance Biotherapeutics è una delle società pubbliche più importanti nel campo della cell therapy per tumori solidi perché ha già superato una soglia che molte piattaforme oncologiche non raggiungono mai: l’approvazione FDA. Amtagvi, cioè lifileucel, ha ricevuto accelerated approval dalla FDA il 16 febbraio 2024 per pazienti adulti con melanoma non resecabile o metastatico già trattati con un anti-PD-1 e, se BRAF V600 positivi, anche con un BRAF inhibitor con o senza MEK inhibitor. L’approvazione conta perché Amtagvi è diventata la prima T cell therapy approvata dalla FDA per un tumore solido, portando la tumor-infiltrating lymphocyte therapy da promessa accademica di lungo periodo a prodotto commerciale reale.

La storia azionaria, però, non è diventata semplice dopo l’approvazione. Anzi, la fase post-approval ha reso il caso più complesso. Prima dell’approvazione il rischio dominante era regolatorio: la FDA avrebbe permesso alla prima TIL therapy di arrivare sul mercato? Dopo l’approvazione, il rischio è diventato operativo: Iovance riesce a produrre, consegnare, rimborsare e scalare una terapia autologa individualizzata nel sistema oncologico reale? Questo è il cuore dell’equity story di IOVA oggi. La società possiede l’asset storico, la posizione di first mover e un’infrastruttura commerciale attiva. Ma deve ancora dimostrare che Amtagvi possa diventare più di un prodotto high-science usato da un numero limitato di centri specializzati.

Questo è il motivo per cui IOVA è interessante per un lettore costruttivo ma disciplinato. Il bull case non si basa su speranza generica. Si basa su approvazione reale, revenue reale, rete crescente di authorized treatment centers, manufacturing interno e pipeline che tenta di estendere la TIL therapy in NSCLC, endometrial cancer, head and neck cancer, cervical cancer, combinazioni frontline melanoma e approcci TIL ingegnerizzati di nuova generazione. La società ha riportato nel 2025 product revenue totale di circa 264 milioni di dollari, inclusi circa 220 milioni da Amtagvi negli Stati Uniti e circa 44 milioni da Proleukin globale, chiudendo il 2025 con circa 303 milioni di dollari di cassa attesi sufficienti a finanziare le operazioni fino al terzo trimestre 2027.

Anche il caso scettico merita rispetto. Iovance ha ridotto le aspettative nel 2025, ha implementato una ristrutturazione e ha dovuto dimostrare che accelerazione delle vendite, miglioramento del margine lordo e disciplina dei costi potessero ricostruire fiducia. Una terapia che richiede resezione tumorale, manufacturing centralizzato, linfodeplezione, supporto con IL-2 e logistica da centro specializzato non è una pillola oncologica o una semplice infusione. Il prodotto può essere clinicamente differenziato, ma il modello commerciale è pesante. Molto della valutazione dipende dalla capacità della società di rendere il percorso più ripetibile, portare più pazienti nel sistema prima e usare l’infrastruttura esistente per sostenere nuove indicazioni.

Il catalyst più vicino è l’aggiornamento Q1 2026 del 7 maggio 2026. Non è un evento FDA binario. È un checkpoint di execution. Gli investitori dovrebbero guardare revenue Amtagvi, contributo Proleukin, margine lordo, turnaround produttivo, attività degli ATC, progresso internazionale, cash runway e qualunque commento aggiornato su NSCLC, endometrial cancer, frontline melanoma e next-generation TIL. Il catalyst di medio periodo più importante è probabilmente NSCLC. Se Iovance costruisce un percorso registrativo credibile nel lung cancer, la storia passa da “cell therapy approvata nel melanoma” a “piattaforma potenzialmente espandibile in uno dei più grandi mercati dei tumori solidi.”

Lettura editoriale Merlintrader. IOVA può essere trattata con bias costruttivo senza diventare promozionale. La società possiede un’approvazione storica e una piattaforma potenzialmente espandibile. Il framework corretto non è “vincitore senza rischi”, ma “piattaforma commercial-stage di cell therapy dove l’execution decide se la prima approvazione diventa la base di un franchise più ampio nei tumori solidi.”

Snapshot rapido

| Campo | Lettura attuale |

|---|---|

| Società | Iovance Biotherapeutics, Inc. |

| Ticker | $IOVA, Nasdaq |

| Terapia cardine | Amtagvi / lifileucel, immunoterapia autologa T cell derivata dal tumore. |

| Indicazione approvata | Melanoma non resecabile o metastatico dopo anti-PD-1 e, se BRAF V600 positivo, dopo terapia target BRAF con o senza MEK inhibition. |

| Status regolatorio | Accelerated approval FDA il 16 febbraio 2024; continued approval potenzialmente dipendente dalla conferma del beneficio clinico. |

| Base revenue 2025 | Circa 264 milioni di dollari di product revenue totale: circa 220 milioni da Amtagvi USA e circa 44 milioni da Proleukin globale. |

| Cash runway | Cash position di circa 303 milioni di dollari al 31 dicembre 2025, attesa dalla società sufficiente fino al Q3 2027. |

| Espansione pipeline | NSCLC, combinazioni frontline melanoma, endometrial cancer, cervical cancer, head and neck cancer, engineered TIL e next-generation cytokines. |

| Catalyst vicino | Q1 2026 financial results e corporate update fissati per il 7 maggio 2026 alle 8:30 a.m. ET. |

La tesi centrale: IOVA oggi è una storia di execution

L’errore più facile su IOVA è continuare a leggerla come biotech pre-approval. Quella versione della storia è finita. La società ha già raggiunto il traguardo che rende la piattaforma impossibile da ignorare: la FDA ha permesso a una TIL therapy autologa di entrare sul mercato per un tumore solido. La domanda attuale è diversa. Iovance può convertire quel successo regolatorio in un business duraturo, preservando abbastanza capitale e momentum di pipeline per espandersi oltre la prima label?

Questo cambio di fase è importante per trader e lettori di lungo periodo perché cambia la struttura dei catalyst. Prima dell’approvazione, il titolo poteva essere dominato da documenti FDA, sentiment PDUFA, speculazioni su advisory committee e posizionamento binario. Dopo l’approvazione, il titolo viene giudicato trimestre per trimestre. Contano ricavi, margine lordo, turnaround manufacturing, numero e maturità degli authorized treatment centers, referral dalla community oncology, friction dei payer, operating expenses e curva di adozione dei pazienti. La società non può più vincere la narrativa solo mostrando che la scienza è impressionante. Deve dimostrare che la terapia può attraversare il sistema sanitario in modo ripetibile.

Qui il bull case diventa più maturo. Una tesi costruttiva su IOVA non deve fingere che il lancio sia stato semplice. Non lo è stato. La società ha dovuto ridurre le aspettative 2025, tagliare costi e difendere la runway. Ma lo stesso periodo ha mostrato che la società può comunque generare product revenue significativo, raggiungere la guidance rivista, migliorare il margine lordo e continuare ad avanzare la pipeline. Questo è il setup più interessante: non una commercial success lineare e pulita, ma un lancio ad alta frizione che potrebbe comunque evolvere verso un modello più investibile se la curva operativa migliora.

Per una pagina evergreen, la sintesi è questa: IOVA è uno dei rari nomi biotech dove il dibattito non riguarda più se la piattaforma sia reale in principio. Approvazione FDA, prescribing information, ricavi commerciali e infrastruttura in maturazione rispondono alla prima domanda. Il dibattito è se la piattaforma sia abbastanza scalabile da sostenere un valore aziendale superiore a una storia oncologica di nicchia single-product. Per questo ogni aggiornamento futuro va letto attraverso quattro lenti: adozione commerciale, efficienza manufacturing, espansione pipeline e disciplina finanziaria.

Amtagvi spiegato: cos’è davvero il prodotto

Amtagvi non è un farmaco convenzionale. È una immunoterapia autologa T cell derivata dal tumore. In pratica, il trattamento inizia dal tessuto tumorale del paziente. I tumor-infiltrating lymphocytes vengono estratti, espansi fuori dal corpo e poi reinfusi dopo una linfodeplezione preparatoria, con supporto successivo di IL-2. È un modello molto diverso da anticorpi, checkpoint inhibitors, target therapy orale o chemioterapia standard. La terapia è personalizzata per ogni paziente: questo è uno dei motivi per cui la biologia è affascinante e anche uno dei motivi per cui la logistica è impegnativa.

La logica clinica dietro la TIL therapy è attraente. Il tumore contiene già cellule immunitarie che hanno riconosciuto il cancro. Il problema è che, dentro il tumor microenvironment, queste cellule possono essere insufficienti, soppresse, esauste o incapaci di produrre una risposta durevole. La TIL therapy tenta di raccogliere il riconoscimento immunitario già esistente, amplificarlo massicciamente e restituirlo al paziente in una forma capace di attaccare il tumore con maggiore forza. Per questo la piattaforma Iovance viene letta come possibile ponte tra immunologia personalizzata e manufacturing industriale di cell therapy.

Il setting approvato è melanoma avanzato dopo anti-PD-1 e, se BRAF V600 mutation positive, dopo terapia target BRAF. Questo conta perché si tratta di una popolazione con opzioni residue limitate e forte unmet need. I checkpoint inhibitors hanno trasformato il melanoma, ma non tutti i pazienti rispondono e molti progrediscono. Amtagvi entra nel difficile spazio post-checkpoint, dove una risposta durevole può avere valore elevato anche se il trattamento è intensivo.

L’accelerated approval si basa su objective response rate, e la label chiarisce che la continued approval può dipendere dalla verifica e descrizione del beneficio clinico in trial confermativi. Questo non è insolito per accelerated approvals, ma è importante. IOVA è commerciale, ma la storia regolatoria resta viva. Gli studi confermativi e di espansione non sono decorazione opzionale: fanno parte dell’architettura regolatoria e strategica di lungo periodo del franchise.

Timeline: dalla ricerca alla biotech commercial-stage

| Periodo | Milestone | Perché conta |

|---|---|---|

| Fondazione accademica | La TIL therapy nasce da una lunga storia scientifica, incluso lavoro presso National Cancer Institute e centri oncologici accademici. | Ha dato a Iovance una piattaforma radicata in decenni di ricerca immuno-oncologica, non una modalità completamente speculativa. |

| Sviluppo pre-approval | Iovance ha costruito trial multicentrici, processi proprietari di manufacturing, bioanalytical platforms e infrastruttura per industrializzare TIL. | La value proposition è diventata non solo terapia, ma capacità di renderla commercialmente consegnabile. |

| 16 febbraio 2024 | FDA ha concesso accelerated approval a lifileucel / Amtagvi nel melanoma avanzato dopo anti-PD-1. | Evento definente: prima T cell therapy approvata dalla FDA per un tumore solido. |

| Launch year 2024 | Iovance ha avviato il lancio commerciale USA costruendo la rete di authorized treatment centers e commercializzando Proleukin. | La storia si è spostata da rischio regolatorio binario a execution commerciale. |

| Reset 2025 | Le aspettative di revenue sono state ridotte e la società ha implementato ristrutturazione per migliorare costi e runway. | È stato il grande test di credibilità del lancio: prodotto reale, ma adozione commerciale più difficile del previsto. |

| Risultati FY2025 | Iovance ha riportato circa 264 milioni di dollari di product revenue, revenue Q4 di circa 87 milioni, gross margin Q4 circa 50% e cassa attesa fino al Q3 2027. | Ha mostrato che il lancio era ancora vivo dopo il reset e che le azioni sui costi potevano sostenere la runway. |

| 7 maggio 2026 | Q1 2026 financial results e corporate update. | Checkpoint di execution su revenue, margine, maturità ATC, timing pipeline e cash runway. |

Storia commerciale: cosa deve funzionare

Il ramp commerciale di Amtagvi ha diverse parti mobili. La prima è identificazione del paziente. I pazienti con melanoma avanzato dopo checkpoint therapy possono essere trattati da una rete ampia di oncologi, ma non tutti hanno familiarità profonda con TIL therapy. Iovance ha bisogno di educazione, referral pathways e relazioni con centri. Un paziente può partire da un community oncologist e poi dover essere inviato a un authorized treatment center capace di gestire il percorso. Questo crea più frizione rispetto a una terapia che può essere prescritta e somministrata localmente senza coordinamento complesso.

La seconda parte è attivazione e maturità dei centri. Elencare authorized treatment centers non basta. La vera domanda è quanti centri stanno realmente referendo, resecando, producendo e infondendo pazienti in modo ripetuto. All’inizio di un lancio molti centri esistono sulla carta ma contribuiscono poco volume. Nel tempo, il bull case commerciale richiede che più centri diventino produttivi, più medici costruiscano fiducia e più team comprendano il flow operativo. Per questo il commentary della società su academic ATCs, community ATCs, prossimità dei pazienti e centri esperti è così importante.

La terza parte è il manufacturing. Iovance ha enfatizzato lo Iovance Cell Therapy Center e l’internalizzazione del manufacturing lifileucel. Questo è centrale nel modello di business. Se il manufacturing è lento, costoso o imprevedibile, la crescita revenue diventa più difficile e il margine lordo resta sotto pressione. Se il turnaround migliora, cost of sales migliora e la società può trattare più pazienti con meno colli di bottiglia, il modello commerciale diventa più interessante. La società ha citato un manufacturing turnaround di 32 giorni o meno dall’inbound al return shipment verso gli ATC: è una delle metriche operative da continuare a monitorare.

La quarta parte è rimborso e accesso. Amtagvi è una terapia ad alto valore e alta complessità. Il rimborso deve sostenere sia il prodotto sia il percorso di trattamento. La società ha bisogno di fiducia da parte dei payer, supporto nel workflow ospedaliero e un processo di accesso che non scoraggi i pazienti eleggibili. Un rimborso solido non elimina la frizione, ma rende il sistema più ripetibile. Rimborso debole o confusione operativa rallenterebbero il ramp anche se la logica clinica è forte.

La quinta parte è il messaggio clinico. Iovance ha evidenziato real-world response rates e l’importanza di trattare prima. Se i medici credono che i pazienti possano fare meglio quando arrivano ad Amtagvi prima, dopo meno linee terapeutiche, la società può influenzare il comportamento di referral. Questo conta perché la cell therapy soffre spesso quando i pazienti vengono inviati troppo tardi, dopo progressione o peggioramento del performance status. Un obiettivo commerciale essenziale è quindi non solo aumentare la consapevolezza, ma anticipare il timing di referral nel percorso terapeutico.

Financial snapshot e runway

L’aggiornamento finanziario più importante prima del Q1 2026 è il full-year 2025. Iovance ha riportato nel quarto trimestre 2025 product revenue totale di circa 87 milioni di dollari, in crescita di circa il 30% rispetto al trimestre precedente, inclusi circa 65 milioni da Amtagvi USA e circa 22 milioni da Proleukin globale. Per l’intero anno, product revenue totale è stata circa 264 milioni, inclusi circa 220 milioni da Amtagvi USA e circa 44 milioni da Proleukin globale. La società ha riportato anche gross margin from cost of sales nel Q4 di circa il 50%, riflettendo execution operativa e cost optimization.

Questi numeri contano per due ragioni. Primo, mostrano che Amtagvi non è un’approvazione senza revenue. Il prodotto genera vendite reali. Secondo, mostrano che il lancio ha ancora bisogno di scala. Un anno da circa 220 milioni di dollari di Amtagvi USA è significativo per un primo full launch year in una terapia complessa, ma non prova da solo che Iovance abbia già costruito un franchise oncologico high-margin e self-sustaining. La prossima fase deve mostrare se la revenue può continuare a crescere mentre operating expenses e manufacturing cost si muovono nella direzione giusta.

Anche la cassa è centrale. Iovance ha riportato circa 303 milioni di dollari di cash al 31 dicembre 2025 e ha detto che questa posizione dovrebbe finanziare le operazioni fino al terzo trimestre 2027. Questa runway è importante perché la società deve ancora eseguire il launch growth e avanzare gli studi pipeline. Gli investitori biotech sono sempre sensibili al rischio dilution, ma l’update FY2025 ha dato alla società una finestra più chiara per eseguire prima che la prossima grande domanda di finanziamento diventi urgente.

Il financial bull case è semplice: crescita revenue continua, miglioramento del gross margin e spesa controllata possono estendere la credibilità e ridurre la pressione finanziaria. Il financial bear case è altrettanto semplice: se la revenue rallenta, i margini smettono di migliorare o la spesa pipeline resta pesante, la cash runway può tornare a essere un overhang. L’update Q1 2026 del 7 maggio va quindi letto non come semplice earnings print, ma come health check dell’intero operating model.

Pipeline map: dove IOVA può diventare più di Amtagvi melanoma

La più grande domanda strategica per Iovance è se la TIL therapy possa scalare oltre la prima indicazione approvata nel melanoma. Se la risposta è no, IOVA resta una società oncologica specializzata con un prodotto storico ma limitato. Se la risposta è sì, la società diventa qualcosa di molto più ambizioso: una piattaforma capace di entrare in più tumori solidi con diverse generazioni di prodotti TIL e combinazioni.

NSCLC: la strada di espansione a maggiore impatto

Il non-small cell lung cancer è l’area di espansione più importante perché è un mercato grande e perché la malattia post-checkpoint resta un setting difficile. La pipeline Iovance include approcci lifileucel e LN-145 in NSCLC, incluse coorti IOV-LUN-202 e concetti di manufacturing Gen 3. La società ha descritto dati interim positivi e possibili percorsi registrativi; il mercato continuerà a osservare enrollment, response rates, durability, safety, feasibility manufacturing e timing di eventuali strategie sBLA.

Per i trader, NSCLC è il catalyst che può cambiare la scala della società. Il melanoma valida la piattaforma. Il lung cancer potrebbe espanderla in una discussione commerciale molto più grande. Il rischio è che NSCLC sia biologicamente e operativamente difficile: i segnali devono essere sufficientemente forti da giustificare la complessità del trattamento. Un segnale modesto potrebbe non bastare. Un segnale convincente potrebbe rivalutare tutta la piattaforma.

Combinazioni frontline melanoma

Iovance studia lifileucel anche in combinazione, inclusa la frontline advanced melanoma con pembrolizumab attraverso TILVANCE-301. Questo conta perché il trattamento più precoce può migliorare gli outcome e potenzialmente aumentare il numero di pazienti eleggibili. Conta anche per l’architettura accelerated approval: studi confermativi e strategie earlier-line possono sostenere lo standing regolatorio di lungo termine e la portata commerciale di Amtagvi.

Endometrial cancer, cervical cancer e head and neck cancer

La pipeline include endometrial cancer dopo anti-PD-1, combinazioni nel cervical cancer e setting di head and neck squamous cell carcinoma. Queste indicazioni sono importanti perché testano se TIL therapy possa muoversi attraverso più tumori solidi immunologicamente rilevanti. Alcuni programmi potrebbero non essere valuation-driving quanto NSCLC nell’immediato, ma aiutano a definire la breadth della piattaforma. In una pagina evergreen vanno tracciati come optionality, non come valore garantito.

Next-generation TIL e approcci ingegnerizzati

Iovance sviluppa anche approcci di nuova generazione, inclusi PD-1 inactivated TIL come IOV-4001, PBL therapy, Gen 3 manufacturing e next-generation cytokine support. Qui la storia di lungo termine diventa più speculativa ma potenzialmente potente. L’obiettivo è migliorare potenza, persistenza, manufacturing, safety o esperienza terapeutica. Gli investitori dovrebbero trattare questi asset come upside early-stage finché i dati non maturano.

Pipeline takeaway. L’approvazione Amtagvi prova che Iovance può portare TIL therapy al mercato. NSCLC e frontline melanoma testeranno se la piattaforma può diventare più ampia. Engineered TIL e next-generation cytokines testeranno se la società può continuare a innovare invece di dipendere dalla prima generazione della piattaforma.

Mappa dei catalyst futuri

| Catalyst | Timing / status | Perché conta |

|---|---|---|

| Q1 2026 financial results e corporate update | 7 maggio 2026 alle 8:30 a.m. ET | Checkpoint chiave su revenue Amtagvi, revenue Proleukin, gross margin, cash runway, attività ATC e timing pipeline. |

| Ramp commerciale Amtagvi | Trimestrale | Crescita revenue, patient starts, produttività ATC, referral pattern e reimbursement flow determinano se l’approvazione diventa business scalabile. |

| Manufacturing e iCTC efficiency | Ongoing | Turnaround, cost of sales e internal manufacturing execution guidano gross margin e fiducia nella capacità. |

| NSCLC / IOV-LUN-202 updates | Ongoing / futuri update clinici e regolatori | Percorso di espansione pipeline a maggiore impatto; una strategia credibile nel lung cancer può cambiare la scala di IOVA. |

| Frontline melanoma confirmatory / combination work | Ongoing | Importante per l’architettura regolatoria e commerciale di lungo termine del franchise melanoma. |

| Dati endometrial e cervical cancer | Futuri update clinici | Testano se TIL therapy può espandersi in altri tumori solidi oltre melanoma e NSCLC. |

| Progressi regolatori UK e Australia | Possibili approvazioni anticipate nel primo semestre 2026 secondo commentary societario | Lanci internazionali potrebbero ampliare la base revenue e validare domanda ex-USA. |

| Strategia EMA | Società al lavoro su strategia dopo il ritiro della precedente MAA nel 2025 | L’Europa resta importante ma richiede ricostruzione regolatoria attenta. |

| Next-generation TIL / IOV-4001 | Futuri dati early-stage | Potenziale upside platform di lungo periodo, ma ancora early e data-dependent. |

Il confronto REPL: utile, ma non semplicistico

Il secondo Complete Response Letter ricevuto da Replimune per RP1 più nivolumab nel melanoma avanzato rende IOVA più rilevante nella discussione competitiva, ma il confronto va gestito con precisione. REPL e IOVA si trovano nello stesso quartiere clinico perché entrambe guardano al melanoma avanzato dopo checkpoint therapy. Tuttavia i modelli terapeutici sono molto diversi. RP1 era una proposta intratumorale oncolitica. Amtagvi è una cell therapy autologa approvata che richiede raccolta del tumore, manufacturing, linfodeplezione e supporto IL-2.

Il read-through utile non è che Iovance catturi automaticamente ogni paziente che Replimune avrebbe potuto servire. Sarebbe troppo semplicistico. Alcuni pazienti candidabili a un approccio intratumorale iniettabile potrebbero non essere candidati ideali a una cell therapy complessa. Il read-through corretto è che Iovance guadagna centralità narrativa perché è già approvata e commercialmente attiva in un setting post-PD-1 melanoma ad alto unmet need. Quando un competitor near-market viene ritardato o indebolito, il prodotto approvato diventa più centrale nella conversazione degli investitori.

Questo conta perché la storia IOVA è in parte una storia di leadership di categoria. In un campo dove molte piattaforme oncologiche cercano di dimostrare rilevanza nei tumori solidi, essere primi conta. Ma essere primi è un vantaggio solo se la società continua a eseguire. Il setback di REPL aiuta la narrativa relativa, ma la tesi IOVA resta dipendente da ramp Amtagvi, economics manufacturing, lavoro confermativo ed espansione pipeline.

CEO, management ed execution

La sezione management di Iovance merita più di una breve biografia perché la società oggi viene giudicata meno come biotech discovery-stage e più come piattaforma commercial-stage di execution. La domanda sulla leadership non è soltanto se il team scientifico conosca la biologia TIL. È se l’organizzazione riesca a coordinare manufacturing, medical affairs, payer access, training dei centri, sviluppo clinico, strategia regolatoria internazionale e allocazione del capitale durante un lancio complesso.

Frederick G. Vogt, Ph.D., J.D., serve come Interim President e Chief Executive Officer dal 2021 ed è anche membro del board. È entrato in Iovance nel 2016 e in precedenza ha ricoperto ruoli senior legali e corporate nella società, incluso General Counsel. Il suo profilo è particolare per un CEO di biotech commercial-stage perché combina esperienza legale, regolatoria e corporate development con una lunga storia interna in Iovance. Questo può essere un punto di forza in una società dove strategia regolatoria, proprietà intellettuale, manufacturing agreements, infrastruttura payer e optionality partnership contano molto. Il contrappunto è che la leadership “interim” resta parte della storia IOVA da molto tempo, e investitori di lungo periodo possono ragionevolmente voler capire se il board formalizzerà o modificherà la struttura di leadership man mano che la società matura commercialmente.

Anche il broader executive team è importante. I partecipanti alla call Q4 2025 includevano Chief Financial Officer Corleen Roche, Chief Commercial Officer Daniel G. Kirby, Chief Operating Officer Igor P. Bilinsky, Chief Medical Officer Friedrich Graf Finckenstein, Executive Vice President of Clinical Development Brian Gastman, Head of Regulatory and Translational Medicine Raj K. Puri e leadership commercial operations. Questo mix riflette la natura della società: IOVA non è solo una biotech clinica e non è solo una sales story. È contemporaneamente storia di manufacturing, clinica, regolatoria, commerciale e finanziaria.

Per gli investitori, la scorecard del management dovrebbe concentrarsi su execution misurabile invece che su linguaggio ispirazionale. Il primo punto è trasparenza commerciale: il management deve dare abbastanza dettagli su revenue Amtagvi, domanda pazienti, produttività dei centri, comportamento di referral e friction payer per far capire al mercato se il lancio stia migliorando. Il secondo punto è disciplina manufacturing: turnaround time, utilizzo manufacturing interno, gross margin e cost of sales diranno più sulla viabilità commerciale della piattaforma rispetto a dichiarazioni generiche sulla domanda. Il terzo punto è prioritizzazione pipeline: NSCLC, frontline melanoma, endometrial cancer e next-generation TIL non possono essere tutti ugualmente centrali in ogni momento. Il mercato deve capire dove il capitale viene concentrato.

La ristrutturazione del 2025 è stata uno dei test più chiari della credibilità manageriale. Ha mostrato che la società era disposta ad adattare le spese dopo una launch curve sotto le aspettative, invece di continuare a spendere come se il ramp fosse lineare. Per i lettori bullish, questo può essere letto come disciplina: il management ha accettato la realtà e ha preservato runway fino al Q3 2027. Per i lettori scettici, lo stesso evento può essere letto come prova che le assunzioni iniziali di lancio erano troppo ottimistiche. Entrambe le letture sono legittime. Ora conta se il modello post-ristrutturazione produrrà operating leverage migliore nel 2026.

La sezione management andrà quindi aggiornata dopo ogni call importante. Le domande utili sono pratiche: il management ha quantificato meglio il lancio? Il gross margin è migliorato? La società ha mantenuto o esteso la runway? Ha fornito timing più chiaro su NSCLC? Ha spiegato la strategia regolatoria internazionale riducendo l’incertezza? Ha evitato overpromising? IOVA non ha bisogno di linguaggio promozionale dal management. Ha bisogno di metriche di execution ripetibili.

Institutional ownership, insider context e retail sentiment

IOVA resta una biotech molto seguita con una shareholder base che mescola fondi healthcare specialist, grandi asset manager e index investors, investitori event-driven biotech e retail trader attivi. I dati aggregati stile 13F vanno sempre trattati come ritardati e imperfetti, ma gli screening attuali mostrano che l’interesse istituzionale resta materiale. Fintel, per esempio, elenca centinaia di institutional owners e identifica fra i grandi holder riportati nomi come BlackRock, MHR Fund Management, Vanguard, State Street, Bank of America, Invenomic Capital Management, Morgan Stanley, Goldman Sachs, Long Focus Capital Management e Geode Capital Management.

La presenza di grandi istituzioni non è, da sola, una garanzia bullish. Nel biotech, institutional ownership può riflettere esposizione indicizzata, proprietà passiva, posizioni storiche, risk-taking specialistico, strategie hedged o reporting 13F ritardato. La domanda più utile non è semplicemente “ci sono istituzioni?”, ma se gli investitori healthcare specialist stanno aumentando, riducendo o restando pazienti mentre il commercial ramp si sviluppa. Ogni aggiornamento futuro di questa hub dovrebbe ricontrollare ultimi 13F, filing 13D/13G, Form 4 insider e proxy ownership tables prima di trarre conclusioni.

Anche l’insider context va maneggiato con cautela. Insider buying può essere un segnale forte quando è open-market, significativo e non guidato da piani automatici. Insider selling può essere meno informativo quando è fiscale o plan-based. Poiché IOVA è una biotech commerciale volatile, ownership e insider data non dovrebbero essere usati come prova autonoma di convinzione. Sono solo evidenza di supporto. La storia fondamentale resta revenue, margine, progresso pipeline e runway.

Il sentiment retail è naturalmente più emotivo. I bull tendono a enfatizzare che Amtagvi è già FDA-approved, che la terapia è first-in-class nei tumori solidi, che il secondo CRL di Replimune rende Iovance più centrale nella conversazione post-PD-1 melanoma e che NSCLC potrebbe espandere materialmente l’opportunità. Bear e scettici si concentrano sul reset 2025, complessità del trattamento, rischio dilution, frizione di lancio e possibilità che TIL resti troppo pesante operativamente per un’adozione ampia.

L’approccio editoriale giusto è trattare il sentiment retail come termometro, non come prova. Può aiutare a spiegare volatilità, option activity e attenzione social, ma non può verificare efficacia clinica, probabilità regolatoria o domanda commerciale. Per i lettori Merlintrader, il framework pulito è questo: l’attività istituzionale può mostrare se il denaro professionale resta coinvolto; l’attività insider può rivelare alignment del management se le transazioni sono significative; il sentiment retail può amplificare il movimento; ma il driver durevole resta execution Amtagvi e validazione pipeline.

Copertura analisti e aspettative Wall Street

La copertura degli analisti è importante per IOVA perché il titolo si trova all’incrocio fra biotech commerciale, cell therapy, launch execution oncologica e optionality pipeline. Il consensus può cambiare rapidamente dopo update revenue, sorprese sui margini, variazioni di guidance o nuovi dati clinici. All’inizio di maggio 2026, gli aggregatori pubblici di analyst ratings mostrano in generale una configurazione costruttiva ma cauta: il target medio è sopra il prezzo corrente, ma il range dei target è ampio, segnalando disaccordo su quanto grande possa diventare Amtagvi e quanto valore attribuire a NSCLC e alle altre opportunità pipeline.

Una fonte pubblica aggregata, MarketBeat, indicava 12 price target analisti con media intorno a 8,88 dollari, target massimo 16 dollari e target minimo 2 dollari. Il range è più utile della media. Una dispersione così ampia dice al lettore che Wall Street non sta discutendo solo un piccolo beat o miss trimestrale. Gli analisti stanno discutendo la forma dell’intero modello commerciale. Il limite basso riflette il timore che Amtagvi resti una terapia di nicchia capital-intensive. Il limite alto riflette la possibilità che il lancio migliori, i margini si espandano e la pipeline crei optionality significativa oltre il melanoma.

Gli analisti probabilmente si concentreranno su quattro variabili negli update Q1 2026 e successivi. Primo, revenue Amtagvi: non solo il numero assoluto, ma crescita sequenziale e qualità della domanda. Secondo, margini: se manufacturing interno e cost optimization stanno migliorando visibilmente il profilo finanziario. Terzo, cash runway: se la società riesce a preservare la runway fino al Q3 2027 continuando a finanziare la pipeline. Quarto, timing pipeline, soprattutto NSCLC, perché è l’indicazione più evidente capace di cambiare la scala della società se dati e percorso regolatorio diventano credibili.

Per i lettori, i target degli analisti vanno trattati come indicatori di scenario, non come verità. Un target bullish non rende il titolo sicuro, e un target bearish non invalida la piattaforma. Il valore della copertura analisti è che mostra a cosa il mercato probabilmente reagirà. Nel caso di IOVA, la checklist è abbastanza chiara: accelerazione revenue, produttività ATC, economics manufacturing, update pipeline e rischio finanziamento. Se la società migliora queste metriche, le revisioni degli analisti possono diventare vento a favore. Se le metriche deludono, la stessa copertura può mettere pressione rapida sul sentiment.

Bull case

Il bull case su IOVA parte dal fatto più importante: la piattaforma ha già prodotto un prodotto approvato dalla FDA in un tumore solido. Molte storie oncologiche non arrivano mai così lontano. Amtagvi dà a Iovance una base commerciale reale, identità clinica differenziata e posizione first-mover nella TIL therapy. Se la revenue continua a crescere, il gross margin migliora e la produttività degli ATC sale, il mercato potrebbe iniziare a trattare IOVA meno come “failed launch story” e più come lancio difficile che inizia a maturare.